by midtowng | 9/21/2008 07:23:00 PM

All discussion about the proposed taxpayer-funded bailout of Wall Street banks is centered around the idea of, "If we don't bail them out, they will fail."

It seems no one is asking a much more important question of, "Will this bailout do any good?" Or to take this one step further, "Will this bailout do more harm than good?"

We badly need to consider what history teaches us before we repeat the same mistakes all over again.

Lessons From Hoover

People like to look back on FDR's New Deal as a success story of government intervention. These people ignore two important facts: a) that Hoover repeatedly tried to save the Wall Street banks in the preceding years and failed, and b) by the time FDR became president almost every bank in America had already failed. There was almost nothing left to save.

The first thing to understand is that Hoover was an activist president in regards to the economic crisis.

Many of the most popular New Deal programs were actually started under Hoover. For instance, the Federal Home Loan Bank Act, and the Reconstruction Finance Corporation.

There is a cost to that failure, and that cost is wasted taxpayer money that could have been better used if it was simply directed at the working man and woman.

Lessons from Japan

The most important historical example happened very recently on the other side of the Pacific.

In 1998, Japan decided to "recapitalize" its banks to the tune of 60 trillion yen, or 12% of the GDP of Japan. Just 6 months later another 7.5 trillion yen of taxpayer money was dropped into 15 banks.

These are similar numbers to what is being passed around Washington this week. Which brings up the important question of - how well did the bailout work?

In other words, the public bailout of the big banks was a complete and utter failure.

The Japanese government decided to just throw public money at the problem and it fixed absolutely nothing. This is exactly what the Bush Administration is now proposing, and Congress appears to be ready to go along with this disastrous idea. This article titled "Banks learn nothing" should give you an idea of what we should expect.

So far the record of the bailouts during this crisis has been dismal. For instance, it was the Bush's Administrations attempt to bailout the real estate market that caused Fannie Mae and Freddie Mac to go under. The downfall of Fannie and Freddie caused the downfall of AIG.

Even before the past two weeks, $4,748 for each and every person in America had been committed to bailing out Wall Street. What do we have to show for all that money? Absolutely nothing!

There is a term for this: throwing good money after bad.

The choices we face today aren't between bailing out the banks and not bailing out the banks. The choices we face are to uselessly waste taxpayer money trying to bail out banksters, and failing, or to try an entirely different tactic of repairing the balance sheets of the taxpayer instead.

Unfortunately no one in Washington is offering to do the latter.

It seems no one is asking a much more important question of, "Will this bailout do any good?" Or to take this one step further, "Will this bailout do more harm than good?"

We badly need to consider what history teaches us before we repeat the same mistakes all over again.

Lessons From Hoover

People like to look back on FDR's New Deal as a success story of government intervention. These people ignore two important facts: a) that Hoover repeatedly tried to save the Wall Street banks in the preceding years and failed, and b) by the time FDR became president almost every bank in America had already failed. There was almost nothing left to save.

The first thing to understand is that Hoover was an activist president in regards to the economic crisis.

Indeed, while Hoover fulminated against "socalled new deals," it was Roosevelt who accused the President of "reckless and extravagant" spending, and of thinking "that we ought to center control of everything in Washington as rapidly as possible." Roosevelt's running mate, Congressman John Nance Garner of Texas, 63, even claimed that Hoover was "leading the country down the path of socialism."Doesn't this sound a little familiar? Doesn't this sound like the Democrats accusations against the Bush Administration? It should.

Many of the most popular New Deal programs were actually started under Hoover. For instance, the Federal Home Loan Bank Act, and the Reconstruction Finance Corporation.

the publication of the names of the recipients of loans beginning in August 1932 (at the demand of Congress) significantly reduced the effectiveness of its loans to banks because it appeared that political considerations had motivated certain loans.The best example of Hoover history repeating under the Bush Administration is the current policy of the Federal Reserve swapping treasuries for nearly worthless mortgage-backed securities.

New York Times, October 8, 1931All of these things President Hoover tried, and all of these things failed to save both the real estate market and most of the Wall Street banks.

Real Estate Men On Hoover Plan

Skepticism as to President Hoover's plan to liquidate frozen bank assets was expressed yesterday by Charles G. Edwards, president of the Real Estate Securities Exchange. The exchange deals almost exclusively in real estate bonds, of which it is estimated that $1,500,000,000 at par value are in default throughout the country.

[...]

"President Hoover's financial plan," Joseph P. Day said in part, "is a step in the right direction towards making real estate investment more liquid. The system will make it possible for the Federal Reserve Bank to issue acceptance notes against sound real estate securities, thus stabilizing their values. Real estate mortgages are commonly regarded in banking as frozen assets. The Hoover plan seeks to take these substantial investments from the frozen asset class and give them a recognized value."

There is a cost to that failure, and that cost is wasted taxpayer money that could have been better used if it was simply directed at the working man and woman.

Lessons from Japan

The most important historical example happened very recently on the other side of the Pacific.

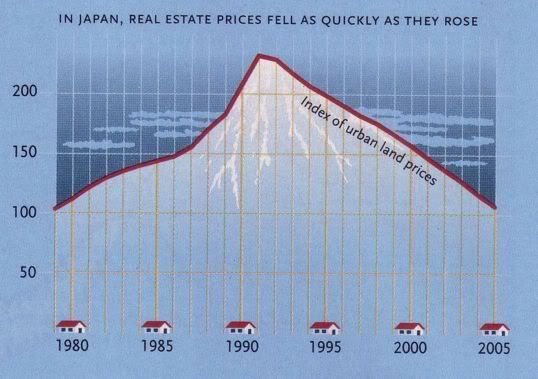

Recognizing that this bubble was unsustainable (resting, as it did, on unrealizable land values - the loans were ultimately secured on land holdings), the Finance Ministry sharply raised interest rates. This popped the bubble in spectacular fashion, leading to a massive crash in the stock market. It also led to a debt crisis; a large proportion of the huge debts that had been run up turned bad, which in turn led to a crisis in the banking sector, with many banks having to be bailed out by the government.Japan's "Lost Decade" is extremely similar to our recent history. It involves an overvalued stock market, an extremely overvalued real estate market, both of which were caused by a near total collapse in lending standards. Initially the Japanese government responded with stimulus packages totaling about 6% of GDP between 1992 and 1993.

Eventually, many become unsustainable, and a wave of consolidation took place (there are now only four national banks in Japan). Critically for the long-term economic situation, it meant many Japanese firms were lumbered with massive debts, affecting their ability for capital investment. It also meant credit became very difficult to obtain, due to the beleaguered situation of the banks; even now the official interest rate is at 0% and have been for several years, and despite this credit is still difficult to obtain.

In 1998, Japan decided to "recapitalize" its banks to the tune of 60 trillion yen, or 12% of the GDP of Japan. Just 6 months later another 7.5 trillion yen of taxpayer money was dropped into 15 banks.

These are similar numbers to what is being passed around Washington this week. Which brings up the important question of - how well did the bailout work?

So far, 25 trillion yen in tax money has been spent, or $238 billion at current exchange rates, on a government overhaul of the financial system, out of $666 billion allocated for that purpose in 1998. Even more has been spent to prop up banks and other financial institutions indirectly, through credit-guarantee programs and the like.

"We are standing at the same divide where we were standing two years ago, when we recapitalized the banks," said Yasuhisa Shiozaki, a youngish legislator from the governing Liberal Democratic Party, who has been a rather lonely advocate of painful financial restructuring. "We can either recapitalize the banks again, or we can just let them go bust."

[...]

Mr. Shiozaki doubts that the government has the will for a second round of refinancing in the wake of Sogo's collapse, when a plan to spend close to $1 billion to waive debt and keep the company afloat was swamped in an outcry of public disapproval.

Ruling-party politicians quickly scrapped the plan, and Sogo failed, blowing away the fig leaf that covered Japan's supposedly resolved bad-debt problems. "What we found out with Sogo and afterward is that the essential and fundamental problems of the Japanese economy were still there or perhaps even worse," Mr. Shiozaki said.

In other words, the public bailout of the big banks was a complete and utter failure.

The Japanese government decided to just throw public money at the problem and it fixed absolutely nothing. This is exactly what the Bush Administration is now proposing, and Congress appears to be ready to go along with this disastrous idea. This article titled "Banks learn nothing" should give you an idea of what we should expect.

It is easy to see that the banks have completely ignored what they should have done. For one thing, they should have cut out the huge retirement allowances; most banks pay 40 to 90 million yen, and some even pay over 100 million yen.Bailout record so far

The government reacted to bad management at these banks by just throwing taxpayers' money at them. Executives at failed banks should not be allowed to get amazingly high retiring allowances. Furthermore, they should be called to account severely. But they are not and couldn't care less, happy in the knowledge that they will get their golden handshake.

In the case of Shinsei Bank, it is almost hard to believe. That bank was started in June last year to take over the management of the Long-Term Credit Bank of Japan which went bankrupt. The government injected 3.6 trillion yen into the bank to erase its bad debts and 240 million yen to help its management.

Just after Shinsei took over the management, the total amount of salaries paid to its executives was 187 million yen. However, this year, it increased to 499 million yen, almost three times more. Also, the average salaries of officers of the Shinsei Bank increased from 482,000 to 499,000 yen.

On the other hand, under the pretext of cleaning up their debt problems, some banks aggressively try to cut off funds to small and medium-scale enterprises.

So far the record of the bailouts during this crisis has been dismal. For instance, it was the Bush's Administrations attempt to bailout the real estate market that caused Fannie Mae and Freddie Mac to go under. The downfall of Fannie and Freddie caused the downfall of AIG.

Even before the past two weeks, $4,748 for each and every person in America had been committed to bailing out Wall Street. What do we have to show for all that money? Absolutely nothing!

There is a term for this: throwing good money after bad.

The choices we face today aren't between bailing out the banks and not bailing out the banks. The choices we face are to uselessly waste taxpayer money trying to bail out banksters, and failing, or to try an entirely different tactic of repairing the balance sheets of the taxpayer instead.

Unfortunately no one in Washington is offering to do the latter.

Labels: midtowng

Permalink

2 Comments:

I haven't read Rauchway's book, but I can tell you if it's by Rauchway, it's excellent. The only one I've personally read -- and I would recommend it -- is Steve Fraser and Gary Gerstle, eds., The Rise and Fall of the New Deal Order. It's a nice collection of essays by major New Deal scholars that covers all the bases, so to speak.

Really great post... reminds me that I need to read up on the Great Depression/New Deal more. Any suggestions- I was thinking of Rauchway's new book on it.